First, the frequency of meetings should be increased, especially in times of crisis, and the level of a few of these meetings enhanced. So, for example, two meetings a year at the head-of-government level and quarterly meetings at the finance-minister level would provide ample time for dialogue...I dont know if Raghuraman Rajan is going for a verbal charade - and at the last minute, spring the BRIC currency. What RRR is suggesting is not going to happen - is clear.Second, the IMF’s permanent Executive Board should be abolished. Important decisions should be vetted by the IMFC and others delegated to IMF management ...

Third, the obvious secretariat is the IMF. Unfortunately, the Fund is not regarded as being impartial, especially by countries that have been seared by its past conditionality. (via Global economy’s dialogue of the deaf- Opinion-The Economic Times).

Showing posts with label global reserve currency. Show all posts

Showing posts with label global reserve currency. Show all posts

Wednesday, June 24, 2009

Global economy’s dialogue of the deaf- Opinion-The Economic Times

Friday, January 30, 2009

Will 2009 be the year of sovereign defaults?

On January 9, Standard & Poor’s announced that Greece, Spain and Ireland were on review for a possible downgrade, indicating that a Eurozone country could default. If financial crises have taught us one thing, it is to take such “black swan possibilities” (as Nicholas Nassim Taleb would describe it) seriously. A sovereign default by a small country could wreak havoc on the markets for credit default swaps (CDS) and might even destroy financial institutions in other Eurozone countries. It could trigger panic rise in bond yields and the threat of contagion could turn into a self-fulfilling prophecy. A far more serious threat would be a cascading series of defaults that would eventually include one or more of the Eurozone’s large countries. The 10th birthday of Eurozone seems to be holding out ominous portents. (via Sunil Kewalramani: Will 2009 be the year of sovereign defaults?).

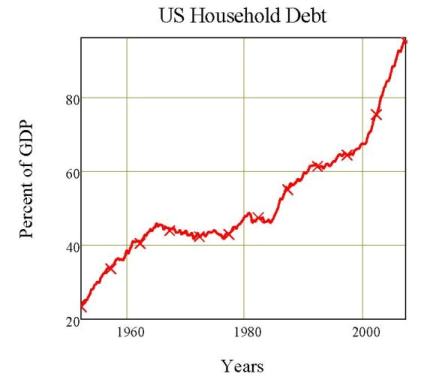

For the last 50 years, under the garb of macro-economic aggregates, total Government finances were seen as proxy for a nation’s economic health. And that assumption, based on faith rather than logic has been been inverted in the last 20 years.

While country and Governmental finances were analysed to within a hair’s breadth away from death, private debt and aggregates of private debt were given a cursory analysis.

As the ‘demand side’ economics crash-landed into the stagflation of the 70s , it gave way to ‘supply side’ economics. With increasing supplies, consumers needed money to buy the supply.

With the arrival of ‘frothy Alan’ and ‘helicopter Ben’ and the ‘ménage à quatre’ was soon complete. The dollar hegemony allowed this build up of debt - and while China is acting as the injured party, it is time someone informed them of the Western concept of ‘caveat emptor’.

The illustration of bathos! Indian policy-bureaucracy complex looking Westward for inspiration.

Tuesday, November 18, 2008

Leadership in the Developing World

Q: Right before this Summit, you said that, “India should get more inclusivity in international financial institutions like the IMF.” What exactly did you put on the table during the Summit? Will restructuring like Bretton Woods possibly expand India’s mandate in the future and in institutions like this?Note the language ...A: I don’t think there is going to be another Bretton Woods Institution. They will give greater representation and voice to developing countries. ... India’s share increased by very small amount but we still think that the developing countries are under represented. Therefore they should have more representation and more voice, which means some other countries, would have to take a haircut. Now whether they will be ready through that I can’t say, they have set the ball rolling now and it would be difficult now to resist any governance reforms on the IMF.(via Moneycontrol >> News >> Economy >> G20 meet sees agreement on common accounting standards: FM)

Describing the G20 summit as "very successful", Prime Minister Manmohan Singh ... said that ... There was one important significance which is clear that the balance of power is shifting increasingly in favour of emerging economies,

"We were previously also invited for the past couple of years for the G8 meetings. But consultations were merely for the sake of form. For the first time there was a genuine dialogue between many of the developed countries and the emerging economies," he said. (via PM terms G20 meet as 'very successful')

This is the language of recipients, of pleading and impotence. Chdiambaram says that 'they' will now "give greater representation and voice to developing countries" Manmohan Singh mirrors the sentiment when he says,"consultations were merely for the sake of form".

The Developing World FTA

Instead of breaking heads with the WTO, the Developing World should declare a 100 country FTA. As Rajat Nag, of the ADB points out,

"East Asia already trades 55% of its output within the region. India’s trade with China, Japan and Asean (Association of Southeast Asian Nations) is increasing. That is the structural shift which will have to happen. Our forecasts are not based on any dramatic shift"

Put the Doha round in deep freeze, and turbo charge work on a FTA within the developing world. That can add another 2%-4% to economic growth - especially to the poorest countries.

The Third Global Reserve Currency

To this add the Third Global Reserve Currency option - and junk the Dollar and the Euro. With this, the World economy will have two strong drivers for economic growth - without dependence on the West. The world needs to move away from the Dollar-Euro duopoly to tri-polar currency regime.

This calls for leadership - intellectual and political. Does the developing world have it? Can India provide it?

Monday, November 10, 2008

Europe throws some bones to the developing world - IHT

Emerging economies want say in financial reforms - International Herald Tribune

European leaders suggested Friday that the International Monetary Fund could also become the worlds financial watchdog, with increased powers to curb financial crises with more money to aid troubled economies.

But Brazil and other emerging-market nations have long complained that their representation in the fund and the World Bank is insufficient. Da Silva said the Group of 20 was better positioned to forge new international financial regulations, because it more broadly represents both rich and developing countries.

Europe wants to stay relevant

Europe which has a major say in the IMF and World Bank, after the USA, obviously wants to increase its role - and decrease US importance. To gets its way, it has gone on a major diplomatic offensive - to the extent of restoring diplomatic ties with Cuba.

To placate the Third World, the duopoly and Europe may show some token resistance - and finally give the Third World some minuscule voting rights. The Third World must not waste time on reforming the IMF and World Bank - but instead focus on setting up a system to manage the Third reserve currency.

As an interim measure, to deal with the current liquidity problem, the US Fed, the IMF and World Bank should be pressured to part with some liquidity.

Why flog the IMF and World Bank dead horses.

Subscribe to:

Posts (Atom)